Welcome to Mortgage Lending Explained, my consumer education blog dedicated to bringing clarity to the mortgage process.

Mortgage Lending Explained is published on Substack at www.JSWhaldo.Substack.com and is also featured here on JSWhaldo.com. Wherever you choose to read, I encourage you to comment, ask questions, and subscribe.

The Mortgage Lending Explained newsletter is published with each new article and podcast episode. My monthly JSWhaldo newsletter focuses primarily on travel and lifestyle content, highlighting new projects and stories from across the site.

After more than 30 years in mortgage underwriting, I write these articles to help consumers understand how mortgage loans really work. My goal is to explain lending in plain English, separate fact from fiction, and provide insight into how mortgage underwriters evaluate loan applications.

Whether you're buying your first home, refinancing, exploring reverse mortgages, or simply curious about credit and lending, I hope you'll find useful information and practical answers here.

Written by J.S. Whaldo, a retired mortgage underwriter with more than three decades of industry experience.

Welcome, and enjoy exploring Mortgage Lending Explained.

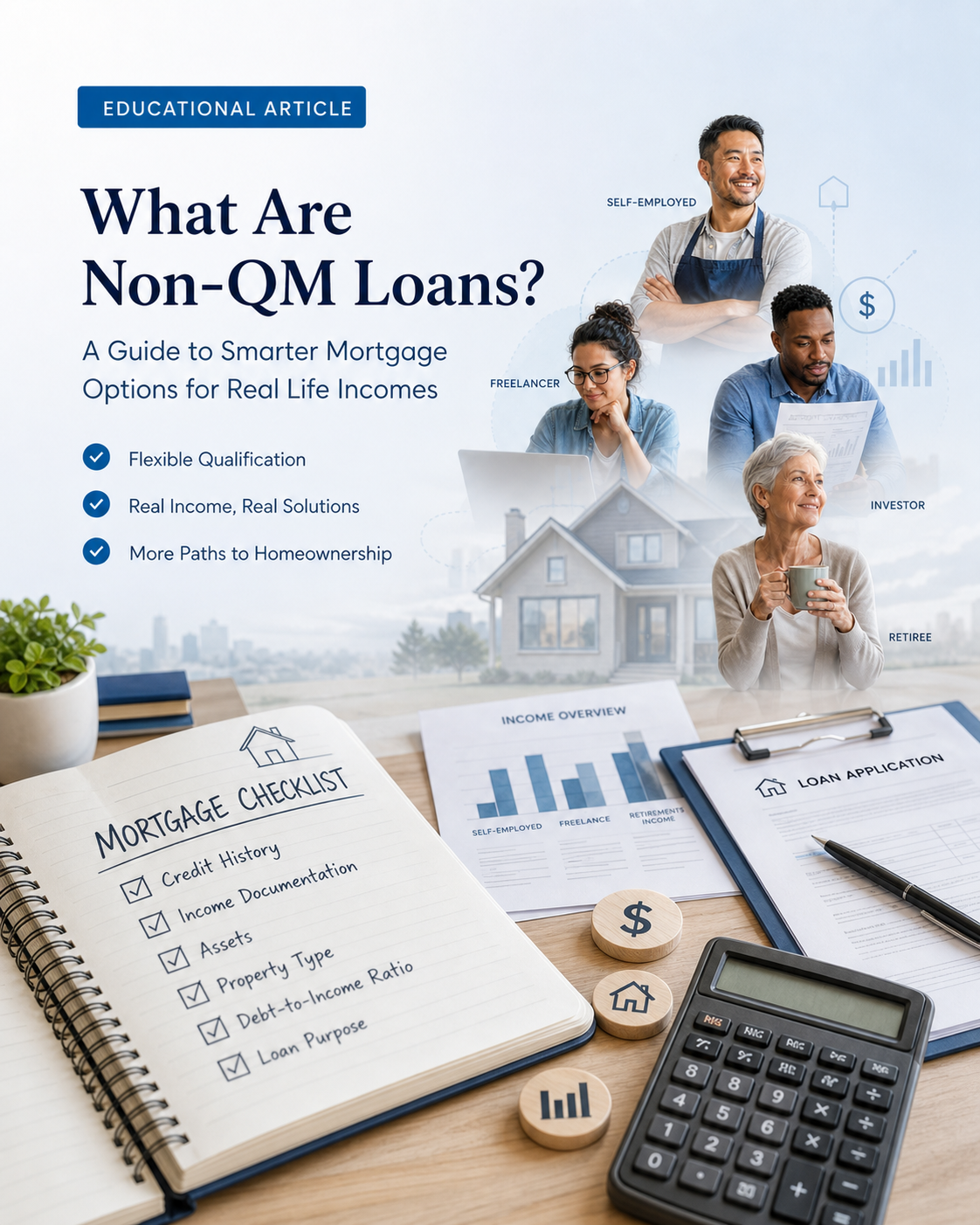

Alternative Mortgage Loans Explained

I’ve spent my career reviewing loan files, and one thing I’ve learned is that financial strength takes many forms. Some people receive paychecks every two weeks. Others own businesses. Some people build investment portfolios. Some spend decades accumulating retirement assets. Everybody’s story looks a little different.

As the workforce has changed, mortgage products have evolved to recognize those differences.

Your Credit Score Is No Longer a Snapshot

A newer scoring model, FICO 10T, is gradually making its way into the mortgage industry and represents one of the more significant changes to credit evaluation I have seen in my career. Unlike traditional scoring models that focus primarily on where a borrower’s credit stands today, FICO 10T looks at how that credit has behaved over time.

What I Learned About Reverse Mortgages as an Underwriter

I have watched reverse mortgages relieve enormous financial pressure for seniors living on fixed incomes. I have also watched adult children discover foreclosure notices taped to the front door of a family home they thought had already been “paid off.”

That is why reverse mortgages are so emotionally misunderstood.

They are neither the financial disaster critics often claim nor the magical retirement solution some advertisements promise. They are simply complicated financial tools that can work very well for some borrowers and very poorly for others.

Why Real Estate Transactions Are Not a DIY Project

From my side of the business, as an underwriter, I could usually tell pretty quickly when a transaction did not involve experienced representation. The files tended to be messier. Communication was slower. Deadlines were missed more often. Small problems grew into larger ones because nobody was truly coordinating the process.

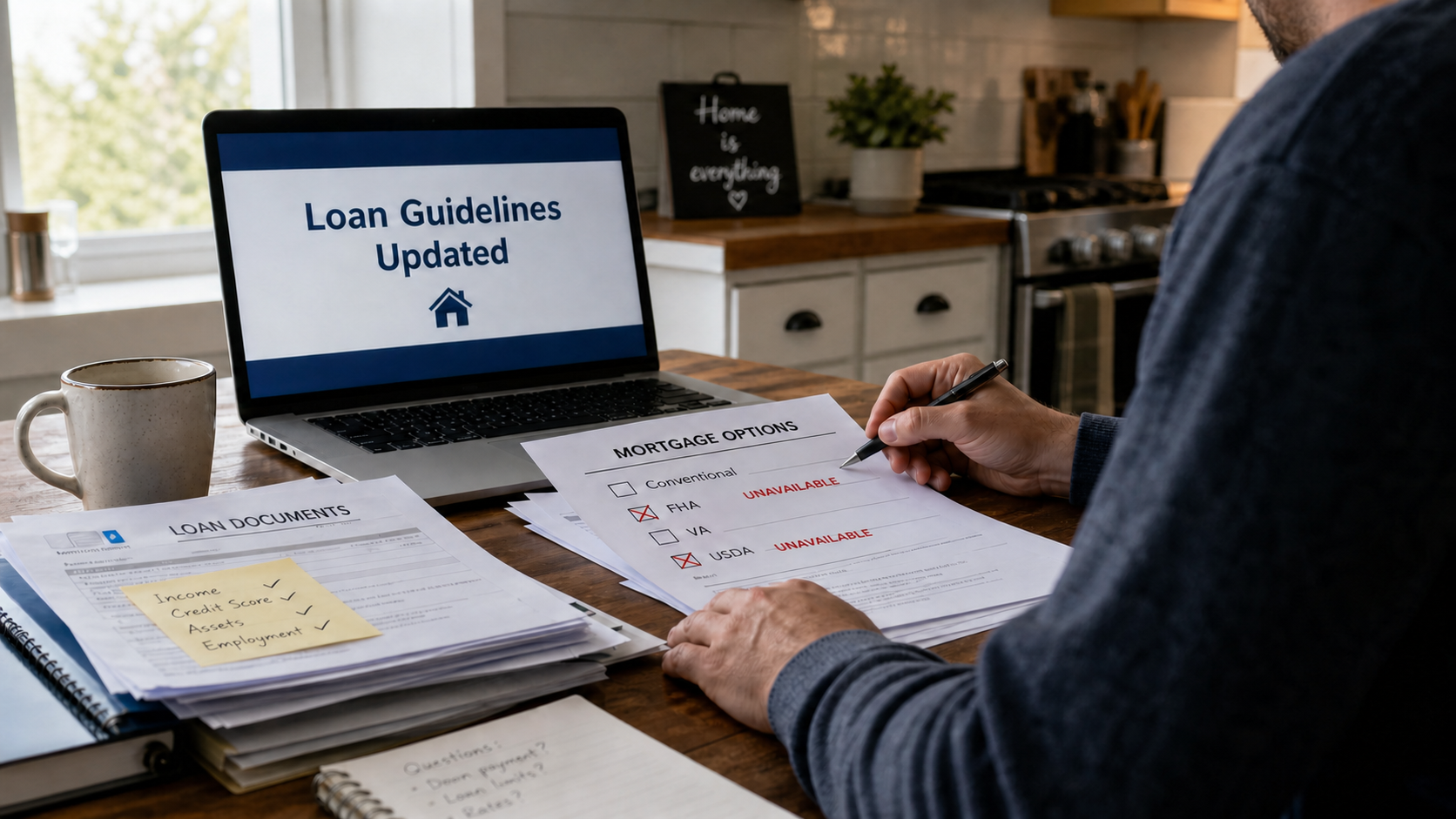

When FHA and USDA Closed the Door on Non-Permanent Residents

Under prior FHA guidelines, legal work authorization, established credit, documented income history, and a proven ability to manage financial obligations were often enough to meet residency eligibility requirements. The new rules changed that standard.

The policy change extends beyond DACA recipients and is also not limited to undocumented borrowers. FHA and USDA restrictions now affect many non-permanent residents living and working in the United States under temporary or renewable immigration status, including DACA recipients and employment-based visa holders in skilled professional roles.

What the New Appraisal Changes Mean for Your Home Value and Loan Approval

One of the biggest shifts is the move toward structured data. Historically, much of the nuance in an appraisal resided in the addendum. That’s where the appraiser explained decisions, provided context, and sometimes clarified things that didn’t fit neatly into a box. In the new format, that kind of open-ended narrative is being pulled into the body of the report itself. Commentary is still there, but it’s tied directly to specific data points rather than sitting at the end as a separate explanation.

What Is a Home Appraisal and Why It Matters More Than You Think

This is where most people are surprised. The appraisal is not just a number at the bottom of the page. It’s a full story about the property and the market around it.

It starts with the basics. The subject property section identifies the home, ownership details, occupancy, and the type of transaction.

You Don’t Need a Credit Score to Buy a Home, But There’s a Catch

It’s important to understand that alternative credit cannot fix a low or poor credit score. If you have a traditional credit report and your score is low, these programs cannot replace it. Alternative credit is only for borrowers who truly do not have a credit score. If you have bad credit, the lender will still review your credit history, and your score and payment history will factor into their decision.

I also want to be clear that I am not talking about subprime lending. There are many types of loans in the mortgage world that are designed for a wide range of financial profiles. I am talking about traditional agency products like FHA, USDA, Fannie Mae, Freddie Mac, and VA.

1031 Exchanges Explained the Way Investors Actually Need to Hear It

A 1031 exchange is a tax rule under Section 1031 of the Internal Revenue Code. It is not a mortgage program.

It allows real estate investors to defer capital gains taxes and depreciation recapture taxes. Notice I didn’t say tax-free. These taxes are deferred, not forgiven.

At its simplest, a 1031 exchange is a swap. One investment property for another.

At its most complex, it allows you to sell one property and later acquire one or more replacement properties, as long as you follow the rules.

Using Passive Income to Qualify for a Mortgage

Passive income can come from a wide range of sources. Social Security, retirement distributions, investment income, royalties, and support payments all fall into this category.

Some of these do not feel passive at all. Social Security is a good example. It represents years of work and contributions. Regardless of how it is labeled, it is treated under the same set of rules as other non-employment income.

Understanding FHA Mortgage Insurance and How MIP Impacts Your Payments

Private Mortgage Insurance applies to conventional loans when the down payment is less than 20 percent. One advantage of PMI is that it can usually be removed once the borrower builds enough equity in the home.

Mortgage Insurance Premium works differently.

MIP is required on all FHA loans regardless of the down payment amount. Even a borrower putting down more than the minimum 3.5 percent will still have mortgage insurance as part of the loan structure.

FHA collects mortgage insurance in two ways. There is an upfront premium paid at closing, and an annual premium divided into monthly installments added to the mortgage payment.

Private Mortgage Insurance Explained for Homebuyers Putting Less Than 20 Percent Down

Private Mortgage Insurance, or PMI, allows buyers to qualify for a conventional mortgage with as little as 3 percent down. For many first-time buyers, this makes homeownership possible years sooner than saving for a 20 percent down payment.

Mortgage insurance is one of the most misunderstood parts of the home loan process. Many homebuyers hear the term during the mortgage application, but are not always sure what it does or why it exists.

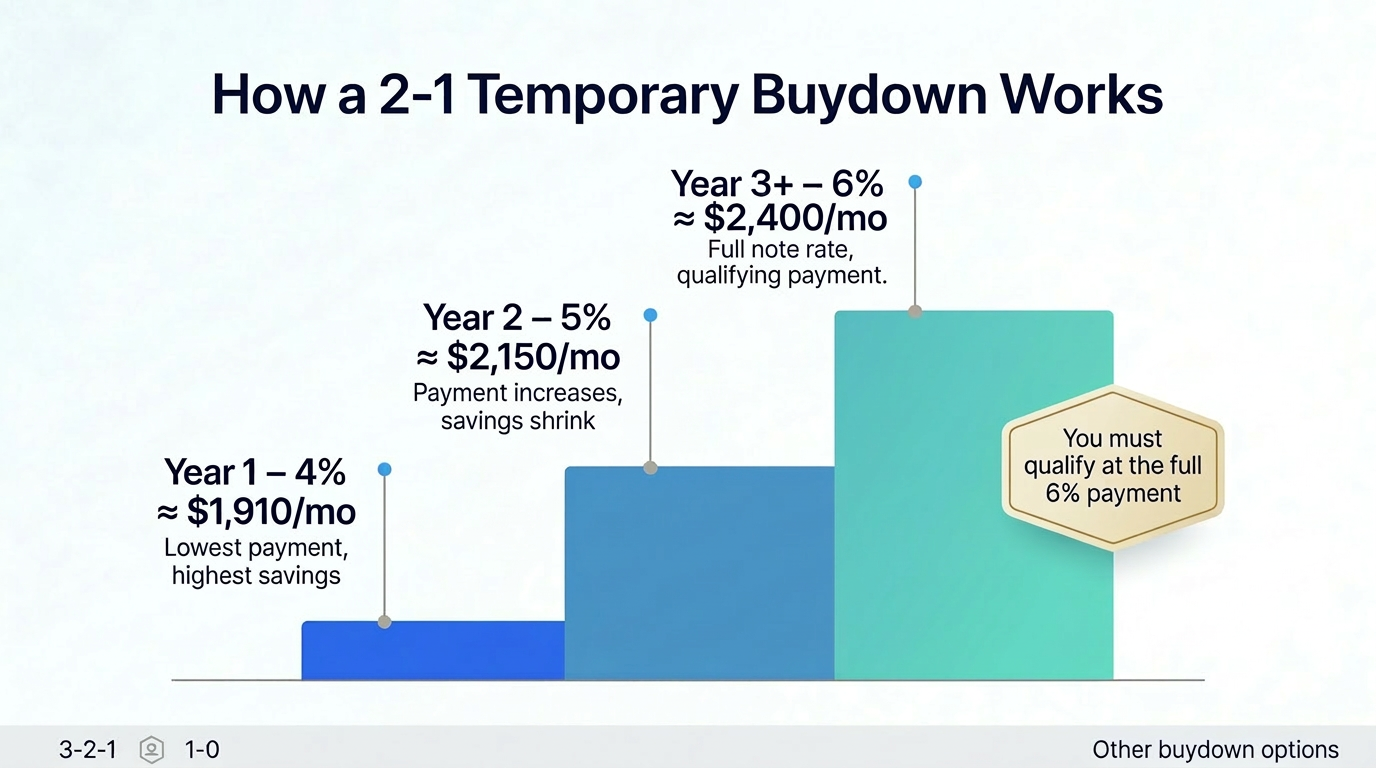

Understanding Temporary Buydowns in Today’s Housing Market

When interest rates climb, the housing industry gets creative.

Products that have quietly existed for decades suddenly show up in headlines, rate sheets, and builder advertisements. One of the loudest right now is the temporary buydown.

Before you assume it is a shortcut around qualification or a gimmick dressed up as affordability, let’s walk through what it actually is and how it really works.

Assumable Mortgage Explained for Today’s Housing Market

What Buyers and Sellers Need to Know About FHA, VA, and USDA Loan Assumptions

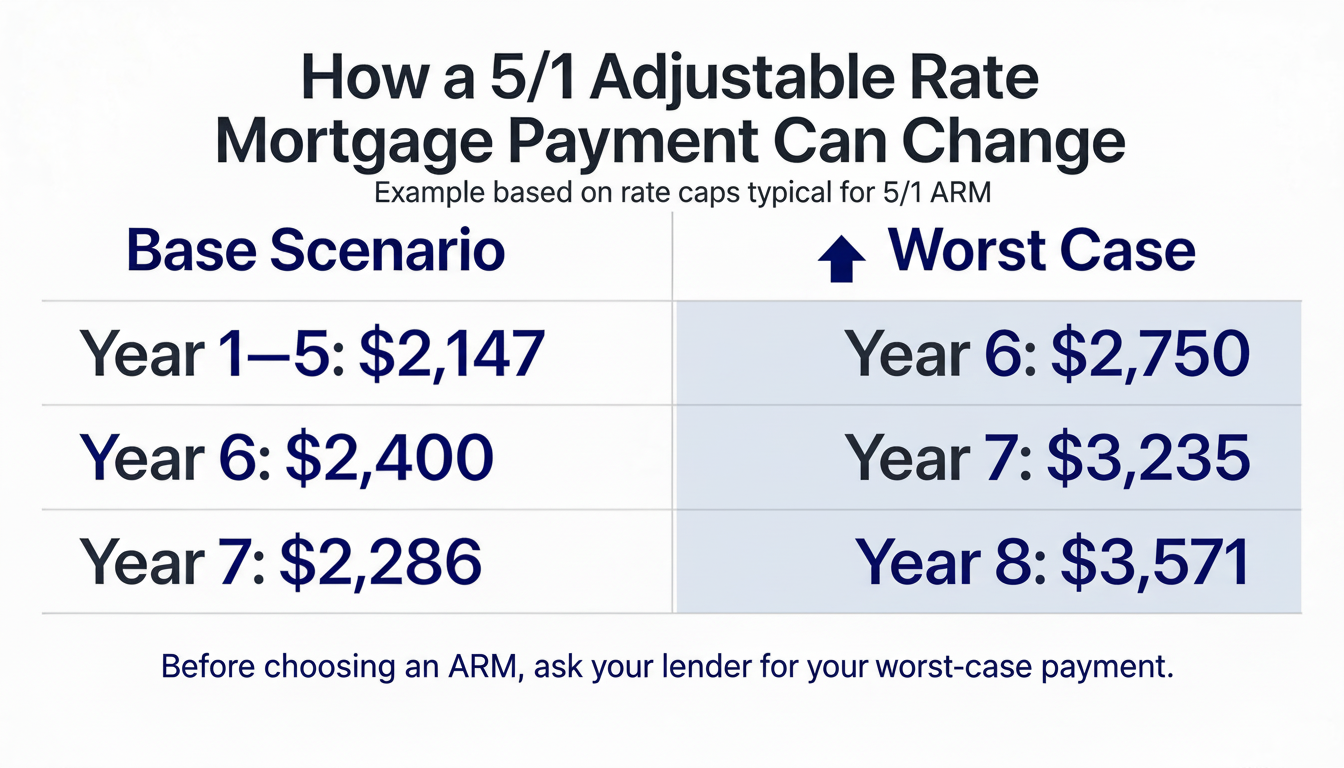

Adjustable Rate Mortgage Explained With Real Payment Examples

What Buyers and Sellers Need to Know About FHA, VA, and USDA Loan Assumptions

Gift Funds for Conventional and VA Loans

The simple, stress-free way to use gift money for a home purchase.

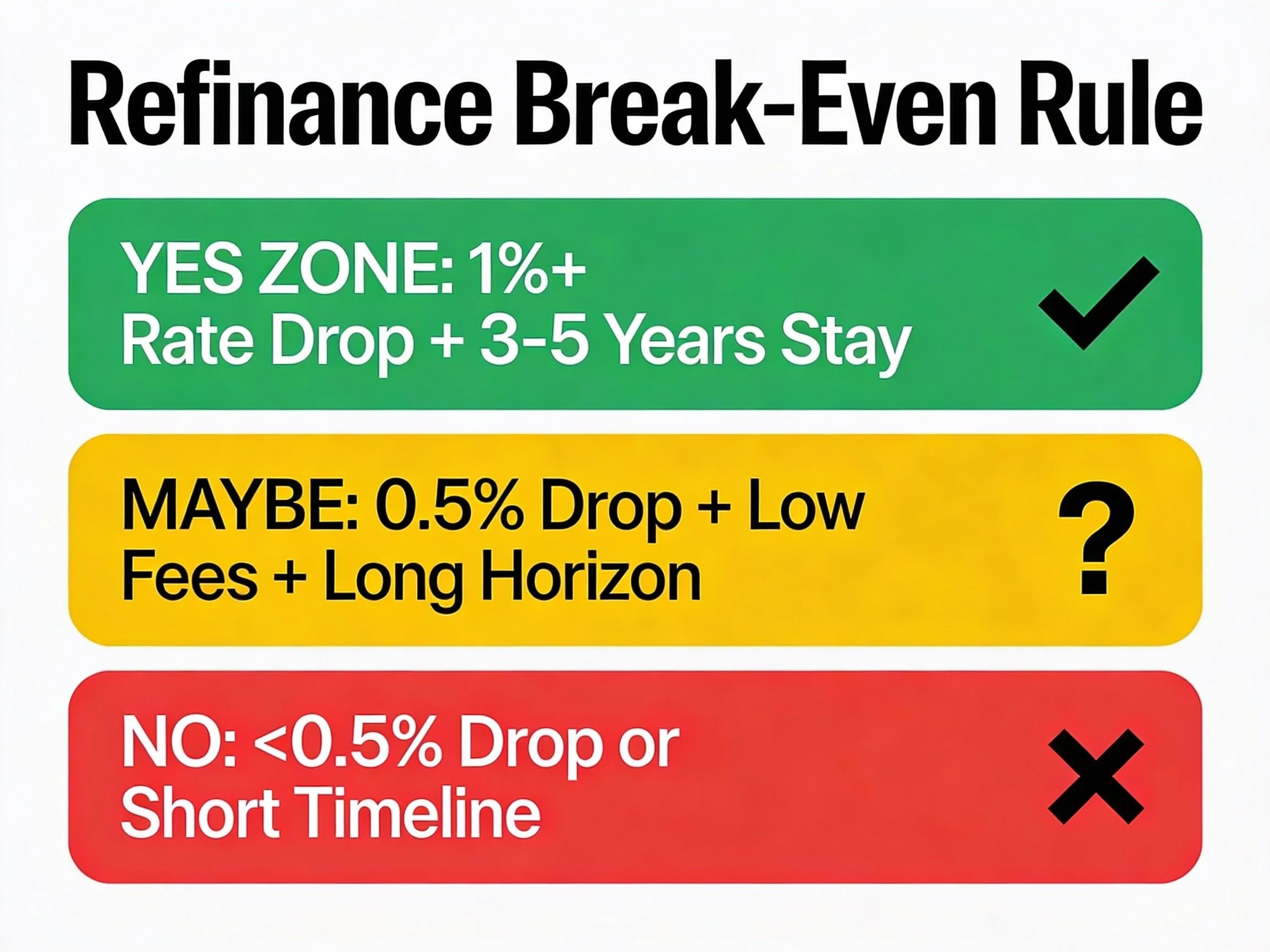

When a Mortgage Refinance Makes Sense and When It Does Not

When does a refinance actually put money in your pocket, and when is it just moving numbers around?

FHA Gift Funds Rules That Can Make or Break Your Mortgage

FHA Gift Fund Rules, Documentation Requirements, and Approved Donors for Smooth Mortgage Closings

Inside the Mortgage Process from Application to Closing

Buying a home is exciting, but the mortgage process can feel like stepping into a house where every door opens to another room you didn’t know existed.

If you’ve ever wondered why the process feels complex or why so many people are involved, this is your guided walk-through of what happens from the moment you apply to the moment your loan closes.

The Holiday Money Moves That Can Kill Your Mortgage Approval

After more than thirty years of underwriting, I can tell you that these little holiday spending choices show up in mortgage files like breadcrumbs. Buy Now Pay Later plans, short-term loans, zero-interest cards, promo-rate balance transfers, all of it adds up. And during the busiest shopping season of the year, borrowers accidentally make their mortgage path harder without realizing they’re doing anything risky at all.