What the New Appraisal Changes Mean for Your Home Value and Loan Approval

What’s behind the new appraisal format, how homes are measured today, and why it matters more than most borrowers realize

Last week, we talked about how appraisals actually work. Not the version people assume, and definitely not the one you see on automated sites. We walked through how value is developed, how comparable sales are used, and why adjustments should be grounded in real data rather than opinion.

What most borrowers don’t realize is that the entire system behind that process is now changing. Not gradually, and not in a minor way. The way appraisals are measured, documented, and reviewed is being rebuilt, and those changes are already underway.

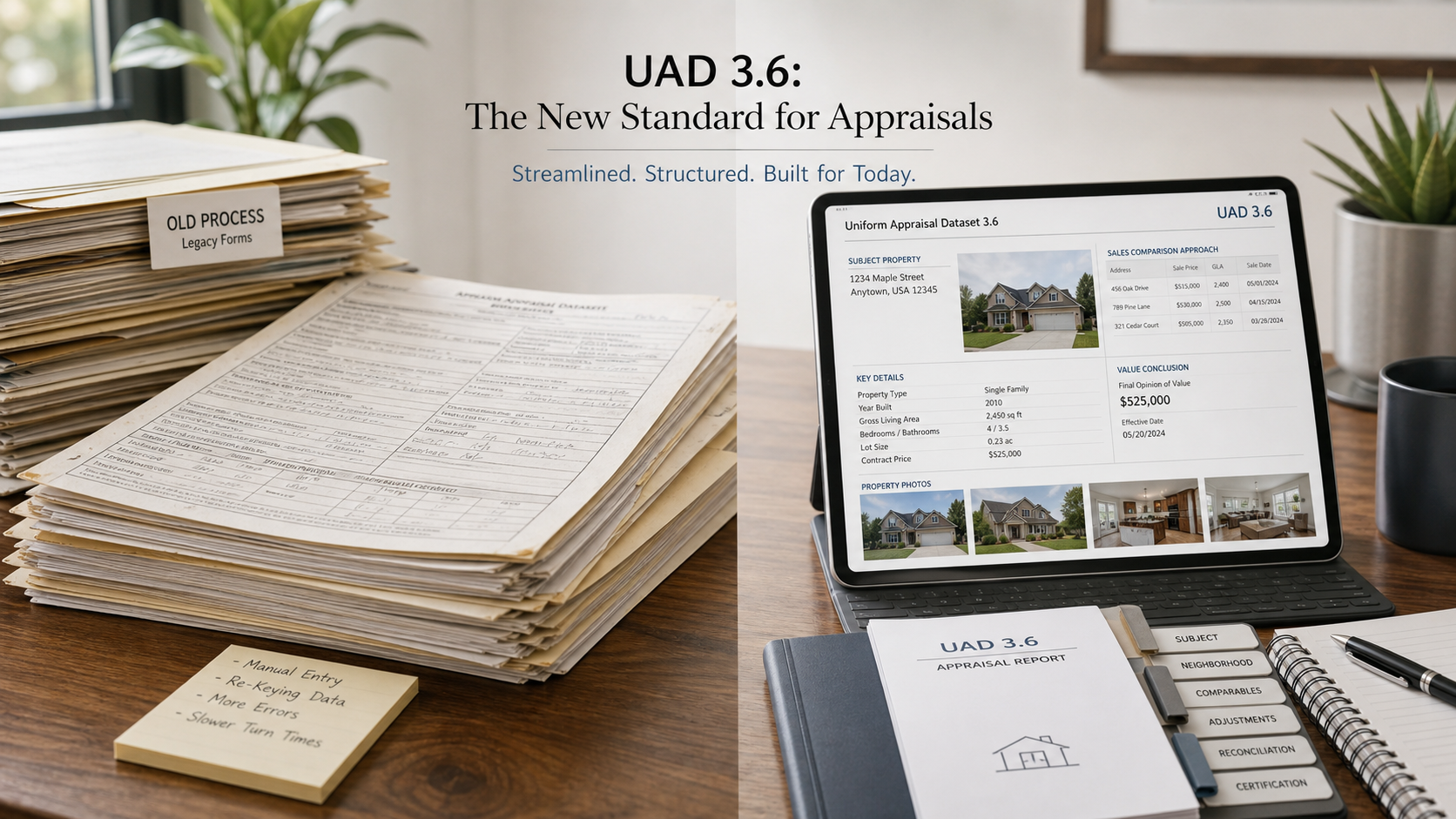

What Is Changing in the New Appraisal Report

Fannie Mae and Freddie Mac are rolling out what’s called the UAD 3.6 update, along with a redesigned Uniform Residential Appraisal Report. This rollout actually started on September 8, 2025, in a limited production phase, during which only certain lenders could begin using the new format. As of January 26, 2026, it opened up to all lenders who are ready to adopt it. The key date to keep in mind is November 2, 2026, when the new format becomes mandatory for all appraisal submissions. After that, the current system, known as UAD 2.6, will be phased out completely by May 3, 2027.

FHA is not far behind. They’ve already announced plans to begin adopting the new format in early Spring 2026, with a full mandate expected around the same time in November 2026. VA and USDA are moving in the same direction, although they haven’t released firm dates yet.

So what is actually changing?

Why Traditional Appraisal Forms Are Being Replaced

For years, appraisals have been built on a set of standard forms. You may have heard them referenced by number, like the 1004 for a single-family home or the 1073 for a condo. Those forms are going away. In their place is a single, dynamic report that adjusts based on the property type and the type of appraisal being performed.

Instead of filling out a fixed form, the appraiser now works through a report that builds itself as the assignment unfolds. Sections appear or disappear depending on whether the property is a condo, a multi-unit, or a detached home, and whether the appraisal is done in person, from the desktop, or through a hybrid approach. It’s a more flexible structure, but it also introduces a level of consistency that hasn’t existed before.

Mortgage Lending Explained is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

How Data-Driven Appraisals Are Changing the Process

One of the biggest shifts is the move toward structured data. Historically, much of the nuance in an appraisal resided in the addendum. That’s where the appraiser explained decisions, provided context, and sometimes clarified things that didn’t fit neatly into a box. In the new format, that kind of open-ended narrative is being pulled into the body of the report itself. Commentary is still there, but it’s tied directly to specific data points rather than sitting at the end as a separate explanation.

At the same time, the report relies much more heavily on predefined fields such as dropdowns, checkboxes, and standardized inputs. This isn’t just about making the report easier to read. It’s about making the data easier to analyze across thousands of appraisals. When information is structured this way, it can be compared, measured, and flagged much more efficiently. That pushes the entire process toward greater consistency, whether the industry is fully ready for that or not.

ANSI Measurement Standards and Why Square Footage May Change

Another important change is the requirement to use ANSI measurement standards for square footage. ANSI, which stands for the American National Standards Institute, is simply a set of standardized rules for measuring a home. It defines what actually counts as living space, how to handle areas like basements or rooms with lower ceiling heights, and how square footage is calculated so that it’s done the same way every time.

While ANSI guidelines have been around for years, this update fully incorporates them into the reporting process. That may sound technical, but it can have very real consequences. If a property was measured differently in the past and is now measured under ANSI standards, the square footage could change. The house itself hasn’t changed, but the way it’s measured has, and that can influence how it’s compared to other properties.

The new report also expands to support different types of appraisals beyond the traditional full interior inspection. Desktop, hybrid, and exterior-only appraisals are all built into the structure. The report adapts to the scope of work, reflecting a broader industry shift toward greater flexibility in how properties are evaluated, especially in lower-risk scenarios.

How the New Appraisal Format Improves Reporting and Transparency

Even the way photos and property details are handled has been updated. Instead of being grouped in one section, they’re now integrated directly into the relevant parts of the report. That makes it easier to connect what you’re seeing visually with the data being presented, and it reduces the chances of important details being overlooked or disconnected from the analysis.

The requirement for the appraiser to drive by all comparable properties and to produce a photo of the comps is being changed. The appraiser can now use photos from the Multiple Listing Service (MLS), Street View, or other reliable sources to document comparable sales rather than driving by them.

What These Appraisal Changes Mean for Homebuyers and Borrowers

All of these changes point in the same direction. The appraisal process is becoming more data-driven, more standardized, and more transparent in how information is presented. That doesn’t eliminate judgment, because appraisal will always involve some level of professional interpretation, but it does narrow the space where unsupported conclusions can hide.

And this ties directly back to something we talked about in the last article. Adjustments in the comparable sales grid are supposed to be based on real, supportable data. If you’re making an adjustment for square footage, it should reflect what the market is actually paying per square foot, and that adjustment should be applied consistently across the report. That isn’t a philosophical stance. It’s fundamental to how valuation is supposed to work.

This new system doesn’t magically fix every issue in the appraisal world, but it does make it harder to rely on vague explanations or inconsistent logic. The structure itself pushes toward a more disciplined approach, which, over time, should lead to more reliable and comparable results.

For borrowers, most of this will happen in the background. You won’t see the form changing in real time, but you may notice differences in how reports look, how square footage is presented, or even the type of appraisal that’s completed on a property. These aren’t random changes. They’re part of a broader shift in how the industry is standardizing the documentation and support of value.

And, as with anything in lending, when the rules around documentation change, the ripple effects tend to show up where people least expect them.