Understanding FHA Mortgage Insurance and How MIP Impacts Your Payments

Mortgage Insurance Premium (MIP) is required on every FHA loan. Here is how it works, how much it costs, and how it compares to PMI on conventional mortgages.

When most homebuyers compare mortgage options, they focus on the interest rate. That makes sense, but it is only part of the story. Mortgage insurance can quietly add hundreds of dollars to a monthly payment and thousands of dollars over the life of a loan.

In the last article, we discussed Private Mortgage Insurance (PMI), which applies to conventional loans. Today, we are looking at the Mortgage Insurance Premium (MIP) for FHA loans. Understanding the difference between these two forms of mortgage insurance can make a meaningful difference in how much a borrower ultimately pays for a home.

In this article, we will walk through how FHA mortgage insurance works, why it exists, how it is calculated, and what it actually looks like in a real loan scenario. Once you understand how MIP is structured, it becomes much easier to decide whether an FHA loan makes sense for your situation.

At this point, many buyers ask a simple question: What is FHA mortgage insurance, and how much does it actually add to a monthly payment?

What Mortgage Insurance Actually Does

Mortgage insurance exists to protect the organization that backs the loan if the borrower defaults. For conventional loans, that protection is required by Fannie Mae and Freddie Mac and ultimately protects the investors who purchase those loans. For FHA loans, the protection comes from the Federal Housing Administration.

Mortgage insurance does not protect the borrower. It protects the loan program that allowed the borrower to qualify with a smaller down payment.

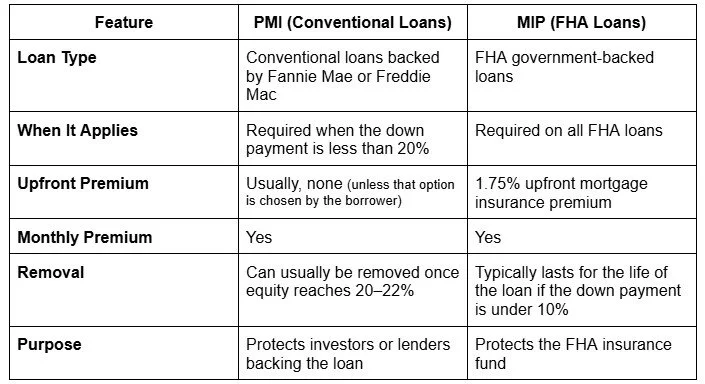

Both PMI and MIP increase the borrower’s monthly mortgage payment. Where they differ is how the premiums are calculated, how long they last, and whether they can eventually be removed.

PMI vs MIP: The Key Differences

Private Mortgage Insurance applies to conventional loans when the down payment is less than 20 percent. One advantage of PMI is that it can usually be removed once the borrower builds enough equity in the home.

Mortgage Insurance Premium works differently.

MIP is required on all FHA loans regardless of the down payment amount. Even a borrower putting down more than the minimum 3.5 percent will still have mortgage insurance as part of the loan structure.

FHA collects mortgage insurance in two ways. There is an upfront premium paid at closing, and an annual premium divided into monthly installments added to the mortgage payment.

Sometimes the easiest way to see the difference is side-by-side.

Mortgage Lending Explained is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

The two parts of the FHA mortgage insurance

FHA mortgage insurance has two components.

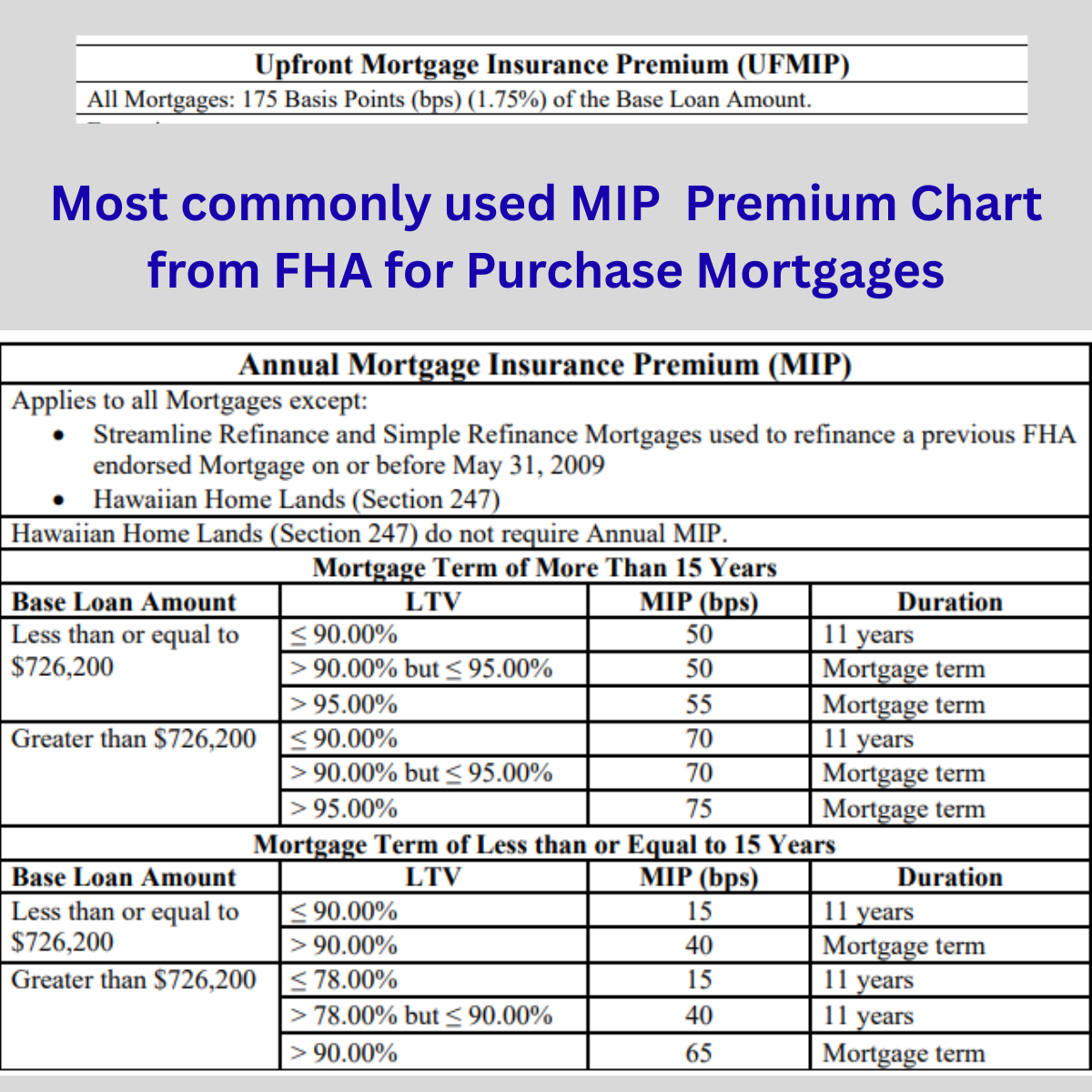

Upfront Mortgage Insurance Premium (UFMIP)

This is a one-time charge equal to 1.75 percent of the base loan amount. Most borrowers finance this into the mortgage rather than paying it in cash at closing.

Annual Mortgage Insurance Premium (MIP)

This is the ongoing insurance cost. It is expressed as an annual percentage of the loan amount but paid monthly as part of the mortgage payment.

The exact annual MIP rate depends on three factors:

• The loan term

• The loan-to-value ratio

• The loan amount

For most borrowers using a 30-year FHA loan with a 3.5 percent down payment, the current annual MIP rate is 0.55 percent of the loan amount.

Example: How Much FHA Mortgage Insurance Costs on a $300,000 Loan

Let’s walk through the numbers using a common FHA scenario.

Purchase price: about $310,880

Down payment: 3.5 percent

Base loan amount: $300,000

Loan term: 30-year fixed-rate mortgage

Upfront Mortgage Insurance Premium

1.75 percent of $300,000 equals:

$5,250

Most borrowers roll this into the loan. When that happens, the starting mortgage balance becomes:

$305,250

Annual Mortgage Insurance Premium

The annual MIP rate for this scenario is 0.55 percent.

0.55 percent of $300,000 equals:

$1,650 per year

Divided into monthly payments:

$137.50 per month

That amount is added to the borrower’s mortgage payment each month along with principal, interest, property taxes, and homeowners’ insurance.

Thanks for reading Mortgage Lending Explained! This post is public, so feel free to share it.

Share

How Long FHA Mortgage Insurance Lasts

This is one of the most important differences between PMI and MIP.

For FHA loans with less than 10 percent down, the annual mortgage insurance remains for the life of the loan.

If the borrower makes a down payment of 10 percent or more, the annual MIP will remain for 11 years.

This is one reason many FHA borrowers eventually refinance into a conventional loan once they have built enough equity in the home.

FHA Mortgage Insurance Rate Chart

FHA publishes a chart that shows the exact mortgage insurance rates based on loan amount, loan term, and loan-to-value ratio.

For most homebuyers using a 30-year FHA loan with a small down payment, the applicable rate will fall into the highest LTV category, currently 55 basis points (0.55 percent annually).

How FHA Loans Compare to VA and USDA Loans

While we are discussing government-backed loans, it is worth noting two other programs.

VA and USDA loans do not require traditional monthly mortgage insurance, unlike FHA and conventional loans.

However, they are not completely free of program fees.

VA loans typically require a one-time funding fee, which helps support the VA loan program. Many disabled veterans and certain surviving spouses are exempt from paying this fee.

USDA loans require both an upfront guarantee fee and a smaller monthly fee. These fees serve a similar purpose to mortgage insurance by supporting the program and offsetting risk.

Pros and Cons of FHA Mortgage Insurance

Like most things in mortgage lending, FHA mortgage insurance has both advantages and tradeoffs.

Pros

FHA loans allow borrowers to purchase a home with a down payment as low as 3.5 percent.

Credit score requirements are generally more flexible than conventional financing.

Because the FHA program insures the loan, lenders are often willing to offer competitive interest rates.

For many buyers, FHA provides a path to homeownership that would not exist with conventional financing.

Cons

FHA mortgage insurance includes both an upfront premium and a monthly premium.

The monthly MIP increases the total housing payment.

For borrowers putting down less than 10 percent, the monthly MIP cannot be removed without refinancing the loan.

In some cases, FHA mortgage insurance may be more expensive than PMI over the life of the loan. One factor in that calculation is that the UFMIP is often rolled into the loan, meaning the borrower pays interest on that amount along with the base loan balance.

Why FHA Mortgage Insurance Exists

One thing I will say about FHA mortgage insurance after many years of underwriting loans is that it is fairly straightforward.

The pricing structure is published and transparent. The variables are limited. Once you know the loan term, loan amount, and loan-to-value ratio, the premium is easy to determine.

The real decision for borrowers is not whether FHA mortgage insurance exists. It always does.

The real question is whether the benefits of the FHA program outweigh the cost of the insurance for a particular borrower.

For many buyers, especially those with smaller down payments or developing credit histories, the answer is yes. FHA can open the door to homeownership years earlier than waiting to save a larger down payment.

Mortgage insurance is rarely anyone’s favorite part of a home loan, but it plays a very real role in making these programs possible. The insurance helps absorb risk, so lenders can approve loans that might not otherwise be approved.

So here is a question I often ask borrowers.

If you were buying today, would you rather wait years to save a larger down payment or move forward sooner with a program like FHA and mortgage insurance?

There is no universal right answer, but I would be curious how you think about that tradeoff.