When FHA and USDA Closed the Door on Non-Permanent Residents

How 2025 guideline changes removed FHA and USDA financing options for DACA recipients, visa holders, and other non-permanent residents

For years, FHA financing provided a path to homeownership for certain non-permanent residents, including DACA recipients and borrowers with valid work authorization. Many qualified the same way any other borrower would qualify: documented income, established credit, acceptable assets, and legal authorization to work in the United States.

That changed in 2025.

How FHA and USDA Loan Eligibility Changed in 2025

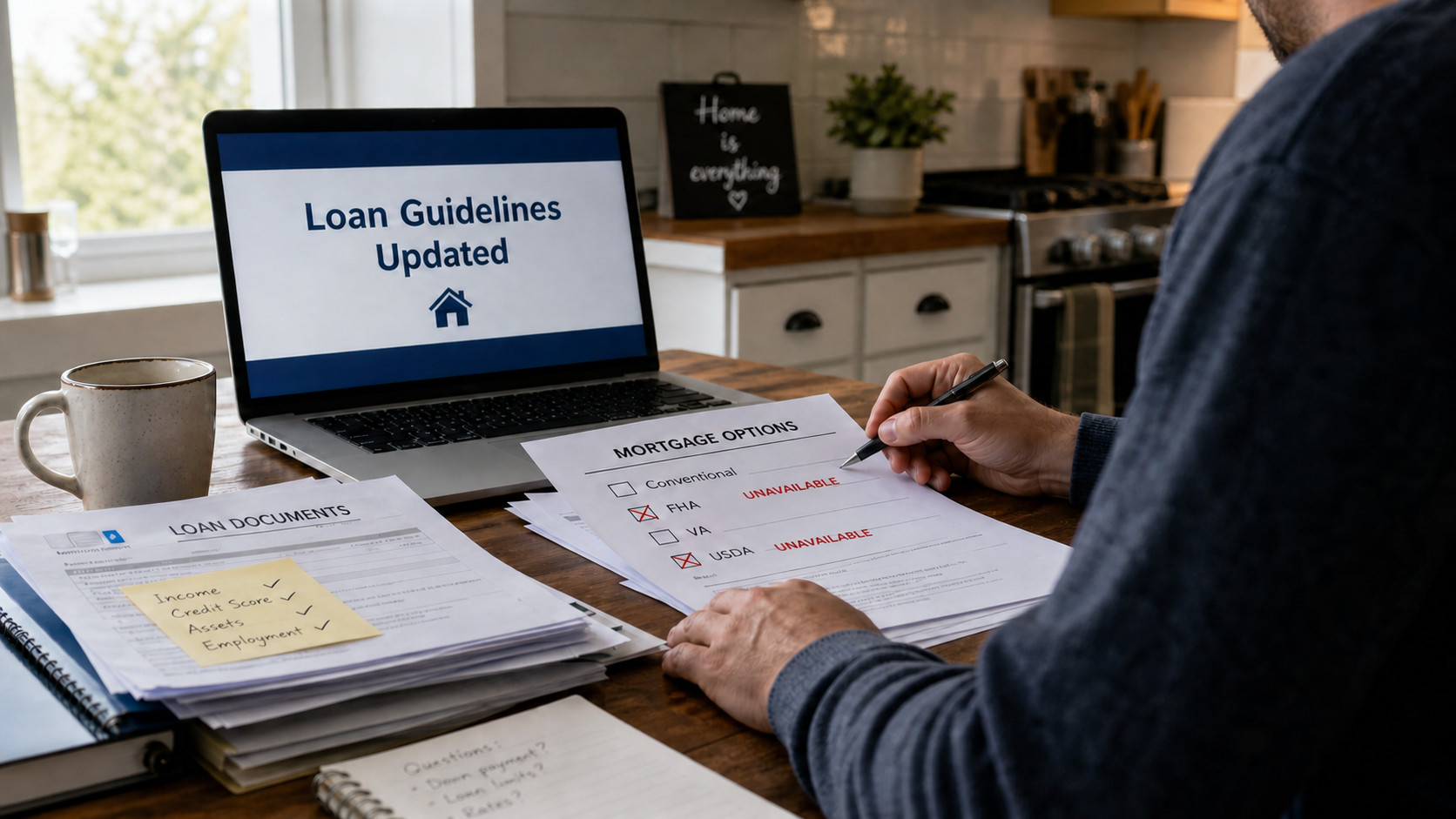

FHA and USDA financing are no longer available to non-permanent residents, even when the borrower has a valid Social Security number, years of tax returns, strong credit, and a documented employment history. The change quietly removed an entire category of otherwise qualified borrowers from two major government-backed mortgage programs.

For many buyers, this news came in the middle of the mortgage process, not before it. The borrower’s credit profile did not change. The guideline did.

In March 2025, HUD issued Mortgagee Letter 2025-09, removing the “non-permanent resident” category from FHA eligibility requirements. The change became mandatory for FHA case numbers assigned on or after May 25, 2025.

USDA adopted similar residency restrictions, limiting eligibility to U.S. citizens and lawful permanent residents.

What DACA Means in Mortgage Lending

One group heavily affected by this change is DACA recipients.

DACA stands for Deferred Action for Childhood Arrivals, an immigration policy created in 2012 that allows certain individuals who were brought to the United States as children to receive temporary protection from deportation and legal authorization to work.

DACA recipients are often called “Dreamers,” although DACA itself is not a path to permanent residency or citizenship. Participants must periodically renew their status and employment authorization.

Mortgage Lending Explained is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Why Non-Permanent Residents Previously Qualified

From a mortgage underwriting perspective, many DACA borrowers historically qualified much like any other wage-earning borrower. They could document income, provide tax returns and bank statements, establish credit history, and verify legal authorization to work in the United States.

Under prior FHA guidelines, legal work authorization, established credit, documented income history, and a proven ability to manage financial obligations were often enough to meet residency eligibility requirements. The new rules changed that standard.

The policy change extends beyond DACA recipients and is also not limited to undocumented borrowers. FHA and USDA restrictions now affect many non-permanent residents living and working in the United States under temporary or renewable immigration status, including DACA recipients and employment-based visa holders in skilled professional roles.

From an underwriting standpoint, these borrowers often looked very similar to traditional borrowers. Many had stable employment, established credit profiles, documented tax returns, and significant reserves. The issue was no longer credit risk in the traditional sense. The issue became residency classification under government loan guidelines.

Mortgage Options Still Available for Non-Permanent Residents

Importantly, this does not mean non-permanent residents cannot buy homes.

Conventional financing through Fannie Mae and Freddie Mac may still be available for certain visa holders and DACA recipients, depending on lender overlays and documentation requirements. Private portfolio and Individual Taxpayer Identification Number (ITIN) loan programs also continue to exist, although these loans often require larger down payments, higher interest rates, or stronger reserve requirements.

In many cases, lender overlays may be more restrictive than the base agency guidelines, making loan shopping especially important for affected borrowers.

The Real-World Impact of Changing Mortgage Guidelines

Mortgage lending has always been driven by guidelines, documentation, and risk analysis. But guideline changes also affect real people making long-term financial decisions. One signature on a policy update can instantly remove financing options that borrowers spent years preparing to qualify for.

Back in July 2025, when John Mackey and I were first building the “Give Me Credit” podcast, John asked me a direct question:

“What’s wrong with the underwriting system? What do you see that, if you could, you could fix?”

My answer came quickly because this is an issue I’ve wrestled with for years.

For borrowers affected by this change, the most important thing to understand is that “not eligible for FHA or USDA” does not necessarily mean “not eligible for a mortgage.” It simply means the path may look very different now.